This is an experimental morning market briefing from my OPUS 4.6 Market Indicator Agent. Please do not take this as market advice; it is a thought experiment to see how agents can assimilate, analyze, and contextualize market and geopolitical events. CAVEAT: Agents make mistakes.

Monday AM Market Briefing — March 2, 2026

1. Overall Warning Level

🔴 CRITICAL — Scenario 3 Materializing: Hormuz Closed, War Widening

The situation has materially escalated beyond the initial assessment. Three developments since the 9:15 AM briefing fundamentally change the outlook:

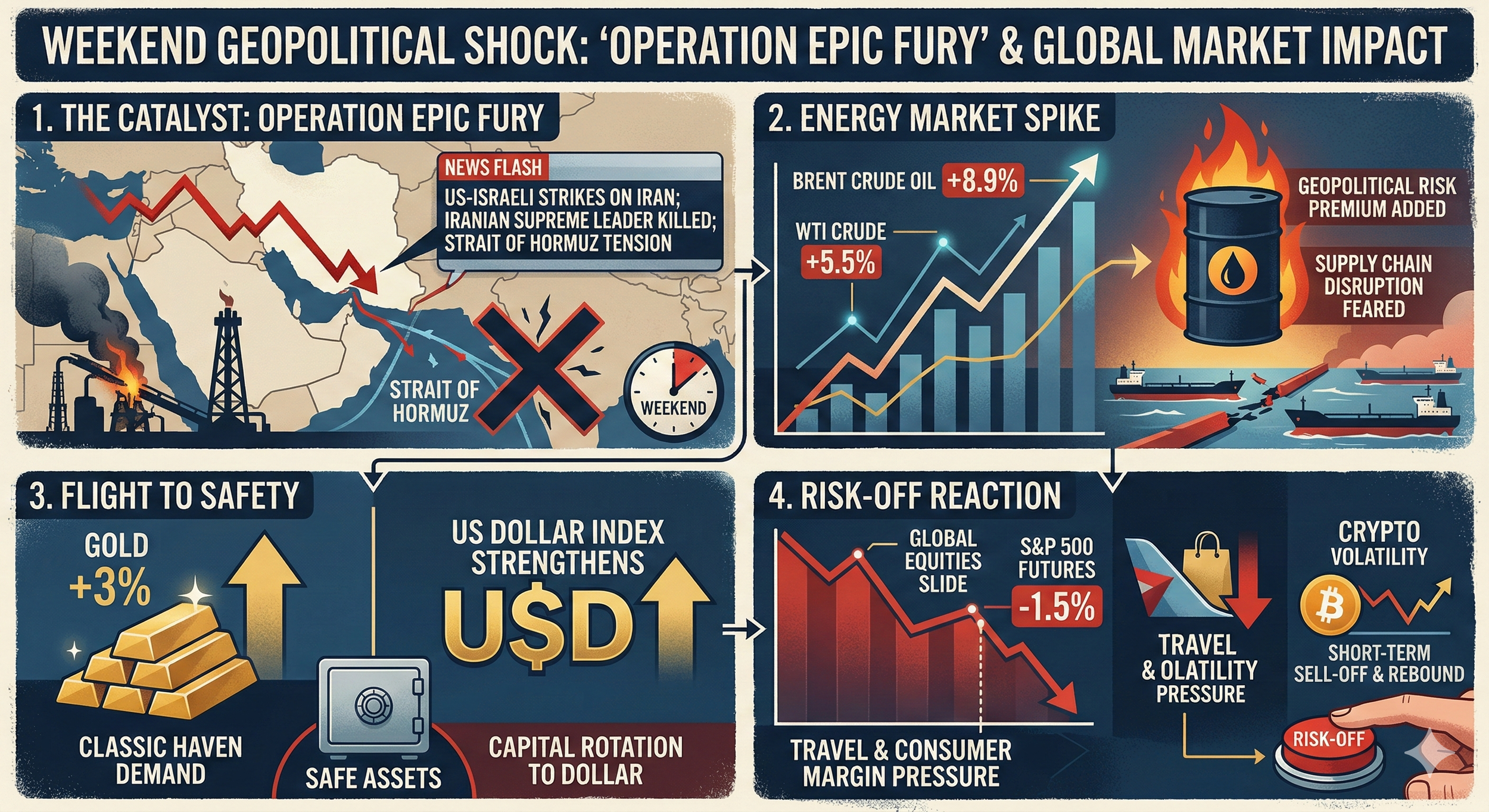

- Strait of Hormuz is effectively closed (per Bloomberg) — this was previously our Scenario 3 tail risk at 20% probability. It is now the base case.

- Ayatollah Khamenei confirmed killed — decapitation of Iranian leadership removes the most likely path to near-term de-escalation.

- War is widening across multiple fronts — Hezbollah has opened a new front with missiles and drones into Israel; Israeli airstrikes on Beirut and southern Lebanon have killed at least 31; Iran's missile/drone attacks now span Bahrain, Iraq, Jordan, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE.

Additional Day 3 developments: 4 US troops confirmed killed in action (CENTCOM). Kuwait accidentally shot down 3 US fighter jets in friendly fire. Iranian Red Crescent reports 555 killed across 131 Iranian cities from US/Israel strikes.

The macro framework stress cluster count is now 7+ red alerts with the Hormuz closure adding a direct stagflation transmission channel. Oil above $80 Brent with Hormuz disrupted means the $90-100+ scenario is no longer a tail risk — it's the near-term trajectory.

2. Core 4 Dashboard

| Indicator | Reading | Status | Δ vs Prior Week |

|---|---|---|---|

| HY OAS | 298 bps (Feb 26) | 🟢 Below 400 ⚠ | +12 bps from 286 (Feb 20) — widening |

| ISM Services PMI | Pending (releases ~Wed Mar 4) | ⚪ Last: above 50 | ISM Mfg due today at 10 AM ET |

| Initial Claims 4-wk MA | ~216K | 🟢 Below 250K ⚠ | Stable (229→208→212K) |

| Hyperscaler Capex | ⚠ AI narrative under pressure | 🟡 Watch | CoreWeave −18.6%, Nvidia negative YTD |

Core 4 assessment: The priority cluster has NOT broken — yet. HY OAS is widening but still well below warning levels. Claims are stable. However, with Hormuz now closed, the probability of a rapid HY OAS repricing toward 400 bps has increased substantially. Credit spreads were already "starting to crack" per Seeking Alpha's Mar 1 analysis. The combination of oil above $80 (heading toward $90+), a widening multi-front war, and the loss of the diplomatic off-ramp (Khamenei's death) means the credit market repricing catalyst is no longer hypothetical. Watch HY OAS daily this week — a gap above 350 bps would signal the break is imminent.

3. What Changed This Week

🔥 Event-Driven: Iran War — Day 3 (Updated)

- US/Israel joint strikes continuing — new wave of attacks on Tehran reported by Israeli military Monday morning

- Iran retaliating broadly — missiles/drones hitting Israel + US/allied assets across 8+ countries

- Hezbollah has entered the war — missiles and drones fired at Israel; Israeli airstrikes on Beirut killing 31+

- Strait of Hormuz effectively closed (Bloomberg) — ~20% of global oil in transit. This was previously our Scenario 3 tail risk

- Khamenei confirmed killed — removes key diplomatic off-ramp

- 4 US troops KIA; Kuwait friendly fire downed 3 US jets; 555 Iranian civilians reported dead

Revised scenario assessment:

Scenario 2 — prolonged regional conflict (was 45%)→ now Scenario 3 — regional war with energy disruption (now 55-60% base case)- Scenario 4 — broader escalation involving Gulf state infrastructure (15-20%, up from 5%)

- Scenario 2 — contained conflict without Hormuz disruption (15%, down from 45%) — requires rapid ceasefire that appears unlikely given Khamenei's death and Hezbollah entry

- Scenario 1 — quick de-escalation (<5%, data-preserve-html-node="true" effectively off the table)

Markets — Live Monday Morning (Updated ~9:40 AM ET)

- S&P 500: ~6,809 (−1.0% from Friday close of 6,878.88) — selling has accelerated since the open as Hormuz closure and Hezbollah front sank in

- Dow: ~48,400 area (−1.2%) — futures had pointed to −550 to −800 pts pre-market

- Nasdaq: Under pressure, futures were −1.4% to −2.0% — tech bearing the brunt

- VIX: 23.41+ (+17.9%) — decisively through the 🔴 threshold of 20, likely heading higher as Hormuz news priced in

- Gold: $5,350-5,400 range — new all-time highs, safe haven bid massive

- WTI Crude: $72+ (opened $75, faded, but Hormuz closure should provide a floor and push higher)

- Brent Crude: $80.01 (+9.8%) — surged as high as +13% at the open before settling. With Hormuz closed, the path to $90-100 is now weeks, not months

- Copper: $6.00 (−1.0%) — risk-off weight offsetting supply concern

- US 10Y: ~3.975% — flight to safety vs inflation fear tug-of-war

- EUR/USD: 1.1707 (+0.87%) — dollar weakening

- Global: STOXX −1.91%, FTSE −1.59%, Nikkei −1.35%

Friday Close (Feb 27) Recap

- S&P 500: 6,878.88 (−0.43%) | Dow: 48,977.92 (−1.05%) | Nasdaq: 22,668.21 (−0.92%)

- Hot PPI rattled markets: +0.5% headline, +0.8% core vs +0.3% expected

- Financials crushed: GS −7.6%, AXP −8.2%, Apollo/Jefferies −8-9% on private credit contagion fears

- AI names continued bleeding: CoreWeave −18.6%, Duolingo −14%

- February was worst month in nearly a year: S&P −1.4%

4. Signals at or Approaching Thresholds

🔴 Red Alerts (6 active)

| Signal | Reading | Threshold | Assessment |

|---|---|---|---|

| UMich Sentiment | 56.4 (Jan) | 🔴 < 65 | Deep in red. Feb prelim expected to worsen given geopolitical shock |

| UMich Expectations | 57.0 (Jan) | 🔴 < 65 | Same |

| NAHB HMI | 36 (Feb) | 🔴 < 40 | Builders despondent. 36% cutting prices, 65% using incentives |

| JOLTS Quits Rate | 2.0% (Dec) | 🔴 ≤ 2.0% | Workers frozen — afraid to leave jobs. Lowest voluntary mobility in years |

| RRP | $0.5-16B | 🔴 Near zero | Liquidity buffer completely exhausted. $16B on Feb 27 was month-end window dressing |

| VIX | 23.41 (live) | 🔴 > 20 | Spiked +18% on Iran open. Was at 18.63 Friday close — already flirting with ⚠ |

⚠ Warning Signals (8 active)

| Signal | Reading | Threshold | Assessment |

|---|---|---|---|

| JOLTS Openings | 6.542M (Dec) | ⚠ < 7.0M | Down 966K YoY, accelerating decline |

| Personal Savings Rate | 3.6% (Dec) | ⚠ approaching 3.5% | Monotonic decline: 4.6→4.0→3.7→3.7→3.6. Next reading could breach |

| Conference Board LEI | 5 consecutive declines | ⚠ at 6 declines | One more triggers. LEI fell 1.2% in H2 2025 |

| HY OAS widening | 298 bps, +12 bps/wk | ⚠ > 400 bps | Accelerating — was 286 on Feb 20. Iran could catalyze a jump |

| Hot PPI | +0.8% core (Feb 27) | ⚠ pipeline inflation | Complicates Fed rate cut timeline — stagflation risk rising |

| Financials vs SPX | GS −7.6%, AXP −8.2% (Feb 27) | ⚠ XLF underperformance | Private credit contagion fears — new signal |

| AI/Hyperscaler Capex | Nvidia negative YTD, CoreWeave −18.6% | ⚠ narrative cracking | Not a capex cut yet, but market no longer willing to pay for AI promises |

| WTI Crude | $72+ (live), Brent $80+ | 🔴 >$90 = stagflation risk | Hormuz now closed per Bloomberg. Brent +9.8%, hit +13% at open. Path to $90-100 dramatically shortened — upgrade to 🔴 |

5. Earnings Call Intelligence

No major watchlist companies reported earnings during the week of Feb 24-28. The prior week's signals remain the dominant narrative:

Key themes still reverberating:

- AI monetization skepticism: CoreWeave −18.6%, Duolingo −14% on Feb 27. The market is increasingly demanding proof that hyperscaler capex translates to revenue. Nvidia negative for 2026 YTD despite no guidance cut — the multiple is compressing.

- Private credit contagion: Financials got hammered Feb 27 (GS −7.6%, Apollo/Jefferies −8-9%). The narrative that private credit stress could spill into broader credit markets is live and will likely intensify under war-driven risk aversion.

- Block workforce reduction: Block announced cutting

4,000 jobs (half of workforce) — a significant signal of tech sector belt-tightening that extends beyond AI.

Upcoming earnings this week to watch:

- Target (TGT) — consumer demand, trade-down behavior

- CrowdStrike (CRWD) — enterprise security spend in geopolitically stressed environment

6. Crypto Dashboard

Prices & Market Data (Updated ~9:40 AM ET)

| Asset | Price | 24h Δ | Market Cap | 7-Day Trend |

|---|---|---|---|---|

| BTC | $66,795 | −0.8% | $1.33T | Bounced to $68K on Khamenei news then faded. Still down ~21% in 30 days from $84.6K |

| ETH | $1,967 | −2.5% | $237B | ETH/BTC ratio ~0.029 — multi-year lows. 6 consecutive red monthly closes |

| SOL | $84 | −4.1% | $47.5B | Down 8.1% over 7 days — leading losses among majors |

| Metric | Value | Signal |

|---|---|---|

| Total Crypto Market Cap | $2.33T | Down from $2.35T last week — continuing drain |

| BTC Dominance | 56.0% | Rising — flight to BTC safety within crypto (risk-off) |

| Fear & Greed Index | 10 — Extreme Fear | Was 5 on Feb 22, 8-14 range for 10+ days. Historically contrarian bullish |

| Hash Rate | ~1,070 EH/s | Healthy, stable — no miner capitulation signal |

| Mempool Fees | 1-2 sat/vB | Very low — almost no demand for blockspace |

Crypto Directional Assessment

Net assessment: Bearish, contrarian setup weakening.

F&G has been below 15 for 10+ consecutive days — historically contrarian bullish. But the macro regime just got materially worse. Hormuz closure + multi-front war + Khamenei decapitation means the "hostile macro" override has strengthened significantly. BTC bounced briefly to $68K on the Khamenei confirmation (possible "buy the rumor" on regime change narrative) but couldn't hold it — confirming it remains in risk-asset correlation mode, not digital gold mode.

Notably, BTC is holding up slightly better than the initial briefing suggested ($66.8K vs $65.4K earlier), which may reflect some marginal safe-haven bid from geopolitical instability. But this is fragile.

Key level: BTC $60,000 remains critical — Polymarket prediction contracts cluster around $57K area for tonight, suggesting the market sees meaningful downside risk. If $60K breaks, mid-$50Ks is next.

7. Key Data Releases This Week

| Date | Time (ET) | Release | Why It Matters |

|---|---|---|---|

| Mon Mar 2 | 10:00 AM | ISM Manufacturing PMI (Feb) | First hard data release of the week |

| Wed Mar 4 | 10:00 AM | ISM Services PMI (Feb) | Core 4 indicator. Services = 70%+ of US economy. Below 50 = major escalation |

| Thu Mar 5 | 8:30 AM | Weekly Jobless Claims | 4-wk MA at ~216K |

| Fri Mar 6 | 8:30 AM | BLS Jobs Report (Feb NFP) | January was +130K |

8. Week-Ahead Outlook

Equities

Revised base case (Scenario 3, 55-60%): A 15-25% correction over coming weeks. HY OAS likely breaches 400 bps within 1-2 weeks as oil sustains above $80-90. This breaks Core 4 pillar #1 and significantly raises recession probability. The S&P ~6,809 level this morning likely does not yet fully price Hormuz — watch for further selling as energy desks and credit markets reprice through the week.

If Scenario 4 materializes (broader Gulf infrastructure damage, 15-20%): Bear market territory — S&P toward 5,500-5,800, oil $120+, gold $6,000+.

Key data this week still matters: ISM Manufacturing (today 10 AM), ISM Services (Wed), Jobs Report (Fri) — these will tell us the pre-war economic baseline. If they come in weak, the starting point for absorbing this shock is worse than assumed.

Crypto

BTC holding ~$66.8K but in risk-asset mode. The brief bounce to $68K on Khamenei's death didn't hold, which is telling. If equities accelerate lower on Hormuz repricing, expect BTC to test $60K this week. F&G at 10 remains contrarian bullish on a 3-6 month horizon, but the near-term path is lower.

Key Risks — Updated Priority

- Strait of Hormuz (ACTIVE) — No longer a risk to monitor; it's happening. ~20% of global oil. Duration of closure is now the key variable. Each week closed = oil +$5-10. Market is not yet pricing a prolonged closure.

- Credit market repricing — HY OAS at 298 bps is still "pre-shock." The gap-up to 350-400 likely comes this week as energy costs feed through. This is where the equity correction becomes self-reinforcing.

- War widening — Hezbollah's entry and attacks across 8+ countries mean the conflict perimeter is expanding, not contracting. Each new front reduces the probability of a quick ceasefire.

- Fed policy paralysis — Oil-driven inflation + slowing economy = stagflation trap. Rate cuts get priced out, but the economy needs easing. The Fed has no good options.

Original briefing prepared March 2, 2026 09:15 ET. Updated 09:40 ET with Day 3 conflict developments, Strait of Hormuz closure (Bloomberg), Khamenei death confirmation, Hezbollah entry, revised scenario probabilities, and live market data.

Framework status: 🔴 CRITICAL — upgraded Feb 28, further escalated Mar 2 on Hormuz closure and war widening