Most teams treat product development like a relay race.

Discovery happens. Roadmap updates. Tickets get written. Build starts. Then weeks later, you circle back to customers and find out what they actually need.

The problem? Customer reality and the competitive landscape don't wait for your sprint cycle. They're changing continuously. But legacy processes only update intermittently—because historically, it's been expensive to do otherwise.

At AFINEA Labs, we asked: what if the signal was always on?

So we built an end-to-end agentic workflow that runs three reinforcing loops: signal, roadmap, and build. Agents handle synthesis and execution. Humans steer strategy and make approval calls.

Here's how it works:

Every design partner conversation gets transcribed. A Notion agent extracts structured signal—bugs, feature requests, recurring themes—and links each item back to the specific call it came from. We never lose the thread. We never start discovery from scratch.

A Perplexity-based agent runs weekly competitive sweeps. Product launches, positioning shifts, pricing changes, notable wins. It produces a delta summary of what changed and why it matters. This used to happen "when someone had time." Now it just happens.

Another agent compares competitive updates against our product vision, current roadmap, and known pain points. It generates proposals: threat responses, whitespace opportunities, things customers are actively pulling us toward.

Then a Claude Code agent maps proposals onto the codebase, estimates difficulty, flags risks, and creates GitHub epics with enough structure that the build loop runs without vague requirements.

And nightly? We let the agents play. Claude Code gets 2-3 hours of free time. It picks what's worth working on, writes code, runs tests, follows repo conventions, and produces a PR with a full paper trail. When we wake up, there's often a surprisingly clever PR waiting for review.

This isn't unfettered autonomy. It works because we're strict about verification and checkpoints. Humans own strategy, prioritization, and final approval. Agents own execution, synthesis, and scaffolding. Every item lands through a renewable PR with an audit trail. Tests are first-class artifacts, not afterthoughts.

The deeper idea: product development should be a living system, not a chain of handoffs.

Customer reality continuously distilled. Competition continuously tracked. Code shipping nightly, all verified and reviewable.

The payoff isn't just speed. It's consistency, discipline, focus, with humans spending time where it actually matters.

Carpe Agentem 🔄

#AgenticDevelopment #ProductDevelopment #AI #SyntheticLeverage

Multi-factor Market Analytics

A few weeks ago, I started with a simple question: could my agents help me pull the signal out of the economic noise?

What followed was a daily conversation with Claude that evolved into something I didn't expect.

First, a 10-point framework for tracking over 50 leading indicators of potential market movement. Then the realization that the hard part wasn't finding the data—it was turning technical indicators, credit warnings, corporate earnings calls, policy moves, labour signals, raw materials prices, and geopolitical events into a view you could actually reason over.

And of course, those conversations became an app.

In this video, I walk through what we built:

- A dashboard that compresses complexity without hiding it

- Credit, technical, labor, and macro indicators layered for context

- A risk nerve center with a live pulse that speeds up when signals align

- Briefings that turn raw data into explanation and exploration

- Intelligence views mapping themes to potential opportunities

- Even vessel tracking for shipping chokepoints (work in progress)

All built in days. Part-time. By my Agentic team. With limited supervision. While focused on my day job.

This isn't market advice. It's a thought experiment on how agents can provide financial intuition, and a glimpse of what synthetic leverage looks like when applied to market intelligence.

Carpe Agentem 📊

#AgenticAI #SyntheticLeverage #MarketIntelligence #AI

Some Key Trends to Watch

1. AI Is Shifting From “Model” to System-Level Infrastructure

Core theme: The competitive edge is no longer just smarter models — it’s context, orchestration, reliability, and integration.

Agentic systems & context

Multiple emails emphasize that agents fail without deep context — enterprise knowledge, intent, history, and governance layers are now essential for reliable output. This shows up in discussions of data-agent context layers, MCPs, and “enterprise context intelligence.”

Agentic engineering is evolving through defined “levels,” from autocomplete → context engineering → compounding feedback loops → autonomous agents with verification. Most orgs are stuck at the early levels.

Reliability over vibes

A recurring warning: “vibe coding” collapses at scale. AI-generated code exacerbates quality issues unless teams adopt stricter testing, smaller modules, and aggressive refactoring.

Karpathy’s “march of nines” appears repeatedly: demos reach 90% easily; enterprise-grade reliability requires exponential effort — and most agent workflows collapse below 35% success without discipline.

Signal: AI is entering the execution era. Winners build guardrails, feedback loops, and context layers — not just prompts.

2. Big Tech & Platform Power: Consolidation Around AI Capability

Core theme: Distribution + AI leverage is concentrating power faster than previous tech cycles.

Platform dominance

Meta buys Moltbook 🦞: Meta acquires Moltbook, an AI-agent social network built on OpenClaw, folding the team into Meta Superintelligence Labs. This signals Meta’s interest in agent-native social simulations, not just chatbots.

YouTube surpasses Disney to become the largest media company globally, driven by scale and AI tooling for creators — reinforcing that distribution + AI tooling beats traditional content ownership.

AI vendor realignment

OpenAI secures a multi-cloud split: AWS gets exclusive stateful agent infrastructure, Azure keeps stateless APIs. This formalizes a two-tier AI stack (execution vs inference).

Cursor vs Claude Code vs Codex: AI coding tools are now in open competition, with revenue scale and enterprise contracts becoming decisive. Momentum shifts fast.

Signal: AI is no longer experimental — it’s redefining who controls platforms, workflows, and developer mindshare.

3. Software Engineering Is Being Rewritten by Agents

Core theme: Agents force better engineering hygiene, or everything breaks.

Studies show most coding agents break 75%+ of their own fixes over time unless evaluated across continuous integration, not one-shot benchmarks.

AI forces “optional” best practices (tests, types, small files) to become mandatory. Messy codebases are hostile environments for agents.

Tools emerging focus on:

Automated QA at scale

Agent-safe AppSec (context-aware scanning)

Evaluation frameworks for non-deterministic outputs

Signal: Agent adoption is a forcing function for long-overdue engineering discipline.

4. Infrastructure & DevOps: AI Traffic Is a New Class of Problem

Core theme: AI workloads break assumptions baked into cloud and networking stacks.

Kubernetes launches an AI Gateway Working Group to handle prompt filtering, response validation, token management, and secure egress, treating AI traffic as first-class infrastructure.

Cloudflare expands browser-based crawling APIs and releases a threat report warning of AI-driven, high-throughput attacks that “live off the land.”

Infrastructure tools shift toward:

Immutable, template-driven self-service (Spacelift Templates)

Simplification (“keep it boring”) as systems scale

Hybrid/on‑prem resurgence driven by data sovereignty

Signal: AI is changing not just apps — but networking, security, and ops economics.

5. Security: AI Accelerates Both Defence and Attack

Core theme: AI collapses the time-to-exploit and time-to-patch on both sides.

Defensive acceleration

Claude Opus 4.6 finds more high-severity Firefox bugs in weeks than humans do in months, proving AI’s power for large-scale code audits.

Offensive escalation

Attackers repurpose AI tools (e.g., CyberStrikeAI) for automated vulnerability discovery.

Multiple zero-days (Fortinet, Apple dyld, n8n, VMware ESXi) highlight that AI-assisted recon is now standard for attackers.

Signal: Security advantage shifts to whoever integrates AI first with real operational controls.

6. Crypto & Fintech: Infrastructure, Not Speculation, Is the Story

Core theme: Crypto is quietly becoming payments and rails, not narratives.

Bitcoin behaves increasingly like a geopolitical hedge, rising amid oil shocks and regional instability.

Stablecoins:

USDC flips USDT in transaction volume

Florida passes the first US state-level stablecoin framework

Enterprises diversify away from USD-only exposure

TradFi convergence:

Nasdaq + Kraken build tokenized equity rails

Circle and Stripe race to agent-native payment infrastructure

Signal: The speculative phase is giving way to boring, regulated, high-volume usage.

7. Product, Design & Org Structure: Lean Beats Large

Core theme: AI compresses teams and rewards clarity.

AI-native org charts reduce communication paths by ~96%, compounding speed.

Generative UI and forward-deployed designers cut build cycles from months to weeks.

Relationships, not features, emerge as the last durable moat as AI commoditizes capability.

Signal: Smaller, sharper teams with AI leverage outperform bloated orgs.

AI is no longer about intelligence — it’s about execution, reliability, and integration.

Winners build systems, not prompts

Infrastructure and security are being re-architected for AI traffic

Engineering discipline is no longer optional

Platforms and distribution matter more than raw model quality

Teams get smaller, faster, and more agent-heavy

Macroeconomic Perspective - OPUS HANDLES MY Daily Briefing

This is an experimental morning market briefing from my OPUS 4.6 Market Indicator Agent. Please do not take this as market advice; it is a thought experiment to see how agents can assimilate, analyze, and contextualize market and geopolitical events. CAVEAT: Agents make mistakes.

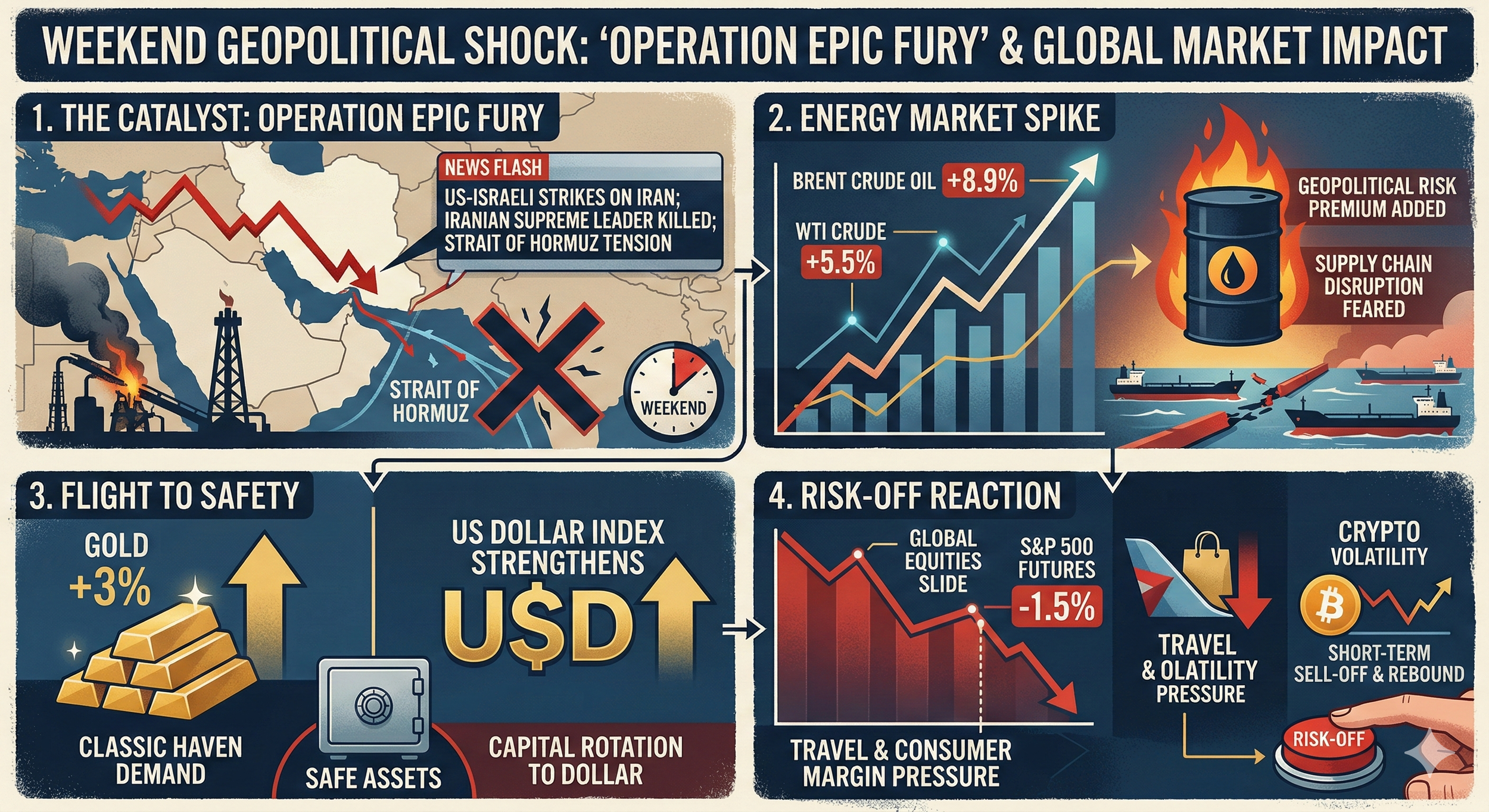

Monday AM Market Briefing — March 2, 2026

1. Overall Warning Level

🔴 CRITICAL — Scenario 3 Materializing: Hormuz Closed, War Widening

The situation has materially escalated beyond the initial assessment. Three developments since the 9:15 AM briefing fundamentally change the outlook:

- Strait of Hormuz is effectively closed (per Bloomberg) — this was previously our Scenario 3 tail risk at 20% probability. It is now the base case.

- Ayatollah Khamenei confirmed killed — decapitation of Iranian leadership removes the most likely path to near-term de-escalation.

- War is widening across multiple fronts — Hezbollah has opened a new front with missiles and drones into Israel; Israeli airstrikes on Beirut and southern Lebanon have killed at least 31; Iran's missile/drone attacks now span Bahrain, Iraq, Jordan, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE.

Additional Day 3 developments: 4 US troops confirmed killed in action (CENTCOM). Kuwait accidentally shot down 3 US fighter jets in friendly fire. Iranian Red Crescent reports 555 killed across 131 Iranian cities from US/Israel strikes.

The macro framework stress cluster count is now 7+ red alerts with the Hormuz closure adding a direct stagflation transmission channel. Oil above $80 Brent with Hormuz disrupted means the $90-100+ scenario is no longer a tail risk — it's the near-term trajectory.

2. Core 4 Dashboard

| Indicator | Reading | Status | Δ vs Prior Week |

|---|---|---|---|

| HY OAS | 298 bps (Feb 26) | 🟢 Below 400 ⚠ | +12 bps from 286 (Feb 20) — widening |

| ISM Services PMI | Pending (releases ~Wed Mar 4) | ⚪ Last: above 50 | ISM Mfg due today at 10 AM ET |

| Initial Claims 4-wk MA | ~216K | 🟢 Below 250K ⚠ | Stable (229→208→212K) |

| Hyperscaler Capex | ⚠ AI narrative under pressure | 🟡 Watch | CoreWeave −18.6%, Nvidia negative YTD |

Core 4 assessment: The priority cluster has NOT broken — yet. HY OAS is widening but still well below warning levels. Claims are stable. However, with Hormuz now closed, the probability of a rapid HY OAS repricing toward 400 bps has increased substantially. Credit spreads were already "starting to crack" per Seeking Alpha's Mar 1 analysis. The combination of oil above $80 (heading toward $90+), a widening multi-front war, and the loss of the diplomatic off-ramp (Khamenei's death) means the credit market repricing catalyst is no longer hypothetical. Watch HY OAS daily this week — a gap above 350 bps would signal the break is imminent.

3. What Changed This Week

🔥 Event-Driven: Iran War — Day 3 (Updated)

- US/Israel joint strikes continuing — new wave of attacks on Tehran reported by Israeli military Monday morning

- Iran retaliating broadly — missiles/drones hitting Israel + US/allied assets across 8+ countries

- Hezbollah has entered the war — missiles and drones fired at Israel; Israeli airstrikes on Beirut killing 31+

- Strait of Hormuz effectively closed (Bloomberg) — ~20% of global oil in transit. This was previously our Scenario 3 tail risk

- Khamenei confirmed killed — removes key diplomatic off-ramp

- 4 US troops KIA; Kuwait friendly fire downed 3 US jets; 555 Iranian civilians reported dead

Revised scenario assessment:

Scenario 2 — prolonged regional conflict (was 45%)→ now Scenario 3 — regional war with energy disruption (now 55-60% base case)- Scenario 4 — broader escalation involving Gulf state infrastructure (15-20%, up from 5%)

- Scenario 2 — contained conflict without Hormuz disruption (15%, down from 45%) — requires rapid ceasefire that appears unlikely given Khamenei's death and Hezbollah entry

- Scenario 1 — quick de-escalation (<5%, data-preserve-html-node="true" effectively off the table)

Markets — Live Monday Morning (Updated ~9:40 AM ET)

- S&P 500: ~6,809 (−1.0% from Friday close of 6,878.88) — selling has accelerated since the open as Hormuz closure and Hezbollah front sank in

- Dow: ~48,400 area (−1.2%) — futures had pointed to −550 to −800 pts pre-market

- Nasdaq: Under pressure, futures were −1.4% to −2.0% — tech bearing the brunt

- VIX: 23.41+ (+17.9%) — decisively through the 🔴 threshold of 20, likely heading higher as Hormuz news priced in

- Gold: $5,350-5,400 range — new all-time highs, safe haven bid massive

- WTI Crude: $72+ (opened $75, faded, but Hormuz closure should provide a floor and push higher)

- Brent Crude: $80.01 (+9.8%) — surged as high as +13% at the open before settling. With Hormuz closed, the path to $90-100 is now weeks, not months

- Copper: $6.00 (−1.0%) — risk-off weight offsetting supply concern

- US 10Y: ~3.975% — flight to safety vs inflation fear tug-of-war

- EUR/USD: 1.1707 (+0.87%) — dollar weakening

- Global: STOXX −1.91%, FTSE −1.59%, Nikkei −1.35%

Friday Close (Feb 27) Recap

- S&P 500: 6,878.88 (−0.43%) | Dow: 48,977.92 (−1.05%) | Nasdaq: 22,668.21 (−0.92%)

- Hot PPI rattled markets: +0.5% headline, +0.8% core vs +0.3% expected

- Financials crushed: GS −7.6%, AXP −8.2%, Apollo/Jefferies −8-9% on private credit contagion fears

- AI names continued bleeding: CoreWeave −18.6%, Duolingo −14%

- February was worst month in nearly a year: S&P −1.4%

4. Signals at or Approaching Thresholds

🔴 Red Alerts (6 active)

| Signal | Reading | Threshold | Assessment |

|---|---|---|---|

| UMich Sentiment | 56.4 (Jan) | 🔴 < 65 | Deep in red. Feb prelim expected to worsen given geopolitical shock |

| UMich Expectations | 57.0 (Jan) | 🔴 < 65 | Same |

| NAHB HMI | 36 (Feb) | 🔴 < 40 | Builders despondent. 36% cutting prices, 65% using incentives |

| JOLTS Quits Rate | 2.0% (Dec) | 🔴 ≤ 2.0% | Workers frozen — afraid to leave jobs. Lowest voluntary mobility in years |

| RRP | $0.5-16B | 🔴 Near zero | Liquidity buffer completely exhausted. $16B on Feb 27 was month-end window dressing |

| VIX | 23.41 (live) | 🔴 > 20 | Spiked +18% on Iran open. Was at 18.63 Friday close — already flirting with ⚠ |

⚠ Warning Signals (8 active)

| Signal | Reading | Threshold | Assessment |

|---|---|---|---|

| JOLTS Openings | 6.542M (Dec) | ⚠ < 7.0M | Down 966K YoY, accelerating decline |

| Personal Savings Rate | 3.6% (Dec) | ⚠ approaching 3.5% | Monotonic decline: 4.6→4.0→3.7→3.7→3.6. Next reading could breach |

| Conference Board LEI | 5 consecutive declines | ⚠ at 6 declines | One more triggers. LEI fell 1.2% in H2 2025 |

| HY OAS widening | 298 bps, +12 bps/wk | ⚠ > 400 bps | Accelerating — was 286 on Feb 20. Iran could catalyze a jump |

| Hot PPI | +0.8% core (Feb 27) | ⚠ pipeline inflation | Complicates Fed rate cut timeline — stagflation risk rising |

| Financials vs SPX | GS −7.6%, AXP −8.2% (Feb 27) | ⚠ XLF underperformance | Private credit contagion fears — new signal |

| AI/Hyperscaler Capex | Nvidia negative YTD, CoreWeave −18.6% | ⚠ narrative cracking | Not a capex cut yet, but market no longer willing to pay for AI promises |

| WTI Crude | $72+ (live), Brent $80+ | 🔴 >$90 = stagflation risk | Hormuz now closed per Bloomberg. Brent +9.8%, hit +13% at open. Path to $90-100 dramatically shortened — upgrade to 🔴 |

5. Earnings Call Intelligence

No major watchlist companies reported earnings during the week of Feb 24-28. The prior week's signals remain the dominant narrative:

Key themes still reverberating:

- AI monetization skepticism: CoreWeave −18.6%, Duolingo −14% on Feb 27. The market is increasingly demanding proof that hyperscaler capex translates to revenue. Nvidia negative for 2026 YTD despite no guidance cut — the multiple is compressing.

- Private credit contagion: Financials got hammered Feb 27 (GS −7.6%, Apollo/Jefferies −8-9%). The narrative that private credit stress could spill into broader credit markets is live and will likely intensify under war-driven risk aversion.

- Block workforce reduction: Block announced cutting

4,000 jobs (half of workforce) — a significant signal of tech sector belt-tightening that extends beyond AI.

Upcoming earnings this week to watch:

- Target (TGT) — consumer demand, trade-down behavior

- CrowdStrike (CRWD) — enterprise security spend in geopolitically stressed environment

6. Crypto Dashboard

Prices & Market Data (Updated ~9:40 AM ET)

| Asset | Price | 24h Δ | Market Cap | 7-Day Trend |

|---|---|---|---|---|

| BTC | $66,795 | −0.8% | $1.33T | Bounced to $68K on Khamenei news then faded. Still down ~21% in 30 days from $84.6K |

| ETH | $1,967 | −2.5% | $237B | ETH/BTC ratio ~0.029 — multi-year lows. 6 consecutive red monthly closes |

| SOL | $84 | −4.1% | $47.5B | Down 8.1% over 7 days — leading losses among majors |

| Metric | Value | Signal |

|---|---|---|

| Total Crypto Market Cap | $2.33T | Down from $2.35T last week — continuing drain |

| BTC Dominance | 56.0% | Rising — flight to BTC safety within crypto (risk-off) |

| Fear & Greed Index | 10 — Extreme Fear | Was 5 on Feb 22, 8-14 range for 10+ days. Historically contrarian bullish |

| Hash Rate | ~1,070 EH/s | Healthy, stable — no miner capitulation signal |

| Mempool Fees | 1-2 sat/vB | Very low — almost no demand for blockspace |

Crypto Directional Assessment

Net assessment: Bearish, contrarian setup weakening.

F&G has been below 15 for 10+ consecutive days — historically contrarian bullish. But the macro regime just got materially worse. Hormuz closure + multi-front war + Khamenei decapitation means the "hostile macro" override has strengthened significantly. BTC bounced briefly to $68K on the Khamenei confirmation (possible "buy the rumor" on regime change narrative) but couldn't hold it — confirming it remains in risk-asset correlation mode, not digital gold mode.

Notably, BTC is holding up slightly better than the initial briefing suggested ($66.8K vs $65.4K earlier), which may reflect some marginal safe-haven bid from geopolitical instability. But this is fragile.

Key level: BTC $60,000 remains critical — Polymarket prediction contracts cluster around $57K area for tonight, suggesting the market sees meaningful downside risk. If $60K breaks, mid-$50Ks is next.

7. Key Data Releases This Week

| Date | Time (ET) | Release | Why It Matters |

|---|---|---|---|

| Mon Mar 2 | 10:00 AM | ISM Manufacturing PMI (Feb) | First hard data release of the week |

| Wed Mar 4 | 10:00 AM | ISM Services PMI (Feb) | Core 4 indicator. Services = 70%+ of US economy. Below 50 = major escalation |

| Thu Mar 5 | 8:30 AM | Weekly Jobless Claims | 4-wk MA at ~216K |

| Fri Mar 6 | 8:30 AM | BLS Jobs Report (Feb NFP) | January was +130K |

8. Week-Ahead Outlook

Equities

Revised base case (Scenario 3, 55-60%): A 15-25% correction over coming weeks. HY OAS likely breaches 400 bps within 1-2 weeks as oil sustains above $80-90. This breaks Core 4 pillar #1 and significantly raises recession probability. The S&P ~6,809 level this morning likely does not yet fully price Hormuz — watch for further selling as energy desks and credit markets reprice through the week.

If Scenario 4 materializes (broader Gulf infrastructure damage, 15-20%): Bear market territory — S&P toward 5,500-5,800, oil $120+, gold $6,000+.

Key data this week still matters: ISM Manufacturing (today 10 AM), ISM Services (Wed), Jobs Report (Fri) — these will tell us the pre-war economic baseline. If they come in weak, the starting point for absorbing this shock is worse than assumed.

Crypto

BTC holding ~$66.8K but in risk-asset mode. The brief bounce to $68K on Khamenei's death didn't hold, which is telling. If equities accelerate lower on Hormuz repricing, expect BTC to test $60K this week. F&G at 10 remains contrarian bullish on a 3-6 month horizon, but the near-term path is lower.

Key Risks — Updated Priority

- Strait of Hormuz (ACTIVE) — No longer a risk to monitor; it's happening. ~20% of global oil. Duration of closure is now the key variable. Each week closed = oil +$5-10. Market is not yet pricing a prolonged closure.

- Credit market repricing — HY OAS at 298 bps is still "pre-shock." The gap-up to 350-400 likely comes this week as energy costs feed through. This is where the equity correction becomes self-reinforcing.

- War widening — Hezbollah's entry and attacks across 8+ countries mean the conflict perimeter is expanding, not contracting. Each new front reduces the probability of a quick ceasefire.

- Fed policy paralysis — Oil-driven inflation + slowing economy = stagflation trap. Rate cuts get priced out, but the economy needs easing. The Fed has no good options.

Original briefing prepared March 2, 2026 09:15 ET. Updated 09:40 ET with Day 3 conflict developments, Strait of Hormuz closure (Bloomberg), Khamenei death confirmation, Hezbollah entry, revised scenario probabilities, and live market data.

Framework status: 🔴 CRITICAL — upgraded Feb 28, further escalated Mar 2 on Hormuz closure and war widening

Macroeconomic Perspective - Agent Update

Last night, I handed my brand-new OpenClaw AI agent a market framework I'd been developing with OPUS 4.6, an early-warning indicator system tracking 50+ leading signals of a market downturn across credit spreads, labour internals, consumer sentiment, housing, volatility, and macro liquidity.

I asked it to review the framework, wire up the data sources, and deliver a briefing every Monday morning.

Within a single session, it:

Pulled live data from FRED, BLS, Census Bureau, and half a dozen other public sources

Calibrated every threshold against current readings and identified 4 red alerts already firing

Built a parallel crypto directional framework covering on-chain fundamentals, derivatives, ETF flows, and sentiment

Mapped ~30 companies across 8 categories for earnings transcript analysis — extracting forward guidance, demand signals, and management tone

Set up a recurring Monday cron job to pull fresh data and deliver a formatted briefing

That was Friday night.

This morning, the US and Israel launched joint military strikes on Iran. Within minutes of me sharing the news, the agent:

Verified reporting across Al Jazeera, CNN, and the Washington Post

Issued a flash briefing with four probability-weighted scenarios

Mapped expected impact on every tracked signal — credit spreads, VIX, oil, gold, crypto, the dollar

Identified the Strait of Hormuz as the key variable separating a correction from a recession trigger

Upgraded the framework warning level from High to Critical

Queued a Sunday evening update timed to futures open

From framework design to live geopolitical crisis response in under 24 hours. No team. No Bloomberg terminal. One person and one agent, over Slack.

The agent isn't just retrieving data. It's synthesizing across macro indicators, earnings intelligence, geopolitical developments, and cross-asset correlations and producing actionable analysis with specific thresholds and scenario frameworks. Work product that used to require a research team and a six-figure data subscription.

We're not at full autonomy. A conversation with OPUS built the framework. I provided the scenario structure for Geopolitical events. And the agent still needs human judgment on the inputs. But the speed of execution, the breadth of integration, and the ability to pivot from a scheduled weekly process to real-time crisis response — that's synthetic leverage applied to market intelligence.

For those of us who've spent careers making decisions under uncertainty, this profoundly changes the toolkit. Not because it replaces judgment. Because it multiplies the surface area of what one person can monitor, synthesize, and act on.

Carpe Agentem.

#AgenticAI #OpenClaw #SyntheticLeverage #MacroEconomics #MarketIntelligence #ImageNanoBanana

Macro Economic Perspectives - An Agent's View

I asked Claude Opus 4.6 to tell me what’s actually happening in the US economy.

Not the headline version. The version that survives a fact check.

It pulled the BLS survey response rates (now down to 43%), found the largest benchmark revision on record (911,000 jobs overstated), identified a two-percentage-point gap between GDP and Gross Domestic Income that historically resolves downward, flagged that long-term Treasury yields are rising through a rate-cutting cycle, and cross-referenced BEA language that Q2 growth “primarily reflected a decrease in imports” — not an increase in output.

Then I did what any analyst should do with work product they didn’t produce themselves: I got a second opinion — a claim-by-claim validation against primary sources from GPT 5.2. Then I asked Claude to rebut. It graciously accepted some of the changes and pushed back on others.

The verdict: a few figures needed updating, some editorial language needed tightening, and one derived calculation got cut because it couldn’t be traced to primary data. But the core thesis — that US economic headlines are being flattered by accounting mechanics, deficit spending, and a deteriorating data collection infrastructure — held up clean.

This is the part that matters: the AI didn’t just retrieve information. It synthesized across data sets, identified methodological weaknesses, and built a structural argument that a second-pass review couldn’t dismantle. That’s analytical work.

Eighteen months ago I would not have trusted these tools to draft an email. Today I’m reasonably comfortable using them to pressure-test a macro thesis.

The full analysis is attached: sourced to BLS, BEA, CBO, and Federal Reserve data. Every claim cited and date-stamped.

Carpe agentem.

#AI #ClaudeAI #Anthropic #MacroEconomics #AgenticAI #Economy

Swarms Go Mainstream

Anthropic just pulled swarms into the core.

Yesterday marked another foundational day in agentic coding. Opus 4.6 dropped, but the bigger story is that agentic teams are now native to Claude Code.

For months, many of us have been parallelizing development through swarms—frameworks and add-ons bolted onto the base offering. Today, Anthropic embraced that trend and pulled it directly into the core product.

And they did it well.

I tested it by giving Claude Code two complex epics from one of my projects—both designed to add full agentic capability to my app. A bit cheeky, I know ... getting agent teams to build agent teams ... whatever ...

What happened next impressed me.

After analyzing the interdependencies across all the GitHub issues, Claude Code broke execution into five sprints. It understood which issues could run in parallel and which had to be completed first. Sprint one: three issues in parallel. Sprint two: two dependent issues. And so on. By sprint five, it parallelized all six remaining issues because there were no interdependencies left.

Each issue is developed in its own work tree. Technically, everything could run simultaneously, but Claude Code was smart enough to avoid the merge-conflict nightmare that would ensue.

The system parsed the problem and allocated work the way a very experienced senior engineer would.

For those of us tracking where the puck is going ... it moved another significant portion up the ice today. The way we built software 18 months ago looks nothing like how we will build it going forward.

For a product guy like me, that's catnip.

Carpe Agentem 🏒

#AgenticDevelopment #ClaudeCode #AI #SyntheticLeverage

Agentic Checkpoint: What can you now build in 15 minutes.

I periodically test the state of the current in coding agents by throwing them a fun project ... and last night I left that exercise quite impressed.

15 minutes. That's how long it took Replit to build a solar storm tracker for me.

Not a prototype. Not a wireframe. A fully functional app with aurora visualizations that shift from deep blues during low radiation to fiery oranges and reds during solar flares. Location search for anywhere in the world. NASA Alerts API integration. 24-hour historical data. A five-day forecast. Even a world map showing current solar activity.

A year ago, this same experiment would have hit what I call the "asymptotic problem"—you get something working quickly, then it just... stops getting better. Without significant handholding, you'd plateau at mediocre.

Not anymore.

What's changed isn't just speed. It's autonomy. The agent found its own bugs. Fixed them. Iterated through solutions. Made aesthetic choices I would have made myself. All while I watched and occasionally nudged.

I've been tracking this shift all year through my work with Claude Code. But seeing how accessible Replit's evolution has made coding crystallized something:

We are no longer technically limited.

For those of us in product, in startups, in building things, the constraint has fundamentally shifted. It's no longer "can we build this?" It's "can we imagine it?"

Think about where the puck was six months ago. Now think about where it'll be in six months.

For the ambitious and the imaginative, there's really no ceiling anymore.

Kudos to Replit for how far they've pushed this. The platform has matured remarkably.

Carpe Agentem.

#AgenticDevelopment #AI #Replit #SyntheticLeverage

Understanding Synthetic Leverage

A year ago, I hadn't written code in 25 years.

Today, I'm shipping software faster than I ever did when coding was my full-time job as a technical co-founder.

Looking back on 2025, I keep returning to one moment: a transatlantic flight where my Claude Code swarm built what would have taken a team 18 developer-days in 6 hours.

That flight forced me to confront something I'd been circling for months: I wasn't coding anymore. I was conducting.

The shift sounds semantic. It isn't.

Coding means writing every line. Conducting means orchestrating agents who plan, build, test, review, and deploy—often going beyond what you explicitly asked for. I've watched them debate approaches among themselves. Implement performance optimizations I hadn't considered. Even leave judgmental comments about code they found elsewhere that "could use improvement."

This is the concept of synthetic leverage that I have been exploring all year. The ability to multiply output without multiplying people.

But here's what took me longer to learn: synthetic leverage requires trust.

We're not quite ready to let agents write all the code, even though they are getting better and better... moving from raw interns to more seasoned developers.

It's because of this that I am now treating agents more as teammates. And the same principles I used to manage human teams apply. Clear context upfront—vision docs, architecture specs, EPICS, etc. Delegation with guardrails, not micromanagement. Regular audits to understand not just what they built, but why. And feedback loops that make the next sprint better than the last.

The agents who've absorbed my coding philosophy through documentation? They make better decisions and gain more autonomy.

The implications are profound:

For founders: A single person can now build and ship rich prototypes in weeks. The barriers to entry have collapsed.

For CEOs with large dev teams: The modern moat is a unique understanding of a problem domain and unmatched execution velocity. You don't get that from just adding more humans.

I've spent my career leading companies from $5M to $500M in ARR, at times, leading thousands of employees. I thought I understood leverage. I didn't. Not like this.

The uncomfortable truth? This isn't about the tools. It's about letting go. Letting agents review each other's work. Letting swarms find solutions you'd never consider. Trusting workflows to enforce standards you might skip.

After a year of building this way, I'm convinced we're witnessing a fundamental shift in how software gets made—and who gets to make it.

The question isn't whether AI will reshape your business. It's about whether you're ready to lead that AI-powered transformational change.

Thanks to the thrilling experience of building again, I know I am back solidly in founder mode ... so stay tuned for an exciting 2026 ... new things are coming!

Carpe Agentem. 🎼

#AgenticDevelopment #AI #StartupLife #SyntheticLeverage #ImageByNanoBanana

Treating Agents Like Teammates

Claude Code and Opus 4.5 have recently made meaningful strides in raising the bar on agentic development. However, I’ve discovered that when you treat the agents more as teammates and less as automatons they really excel.

Let me explain.

Claude Code’s GitHub integration finally lets me manage agents the way a great CTO manages developers: with clear objectives, structured workflows, nuanced guardrails, and most importantly, stable context.

I start every project in Claude Code's planning mode now. The agents and I work together to draft comprehensive plans. I review. We iterate. Then, and this is the key, we instantiate those plans as GitHub epics.

Each epic becomes a container for related issues. Each issue becomes a discrete task with clear objectives, architectural guidelines, and acceptance criteria. The agents work methodically through the issues and submit PRs when done. They even check each other’s work, just like a human team would.

Because Claude Code maintains context through these epics, we’re no longer fighting context window exhaustion. A three-week project stays coherent from day one to deployment. The agents can see the overall arc of the project at any time, track progress, and recall the architectural decisions from week one as they implement features in week three.

The results have been striking. Code quality has improved markedly. The agents are producing more consistent, better-structured code that actually follows our established patterns. Error rates have dropped to levels I’d expect from more senior developers, not the interns agents sometimes seem to channel. And if they stray, I just ask them to revisit the epic and validate whether they’ve delivered against the requirements. They usually course-correct.

With a growing level of comfort, I’m now starting to let the agents monitor GitHub on their own and select their own epics to work on, updating the underlying GitHub issues as they make progress.

They’re not just executing rote tasks anymore—they’re participating in overall project management.

Great tech leaders don’t micromanage. They set clear objectives, establish workflows, remove blockers, and trust their teams to deliver. That’s precisely what I’m doing with my agent teammates now. I’m just applying decades of engineering management wisdom to a new kind of hybrid team. And it’s working.

Carpe Agentem. 🎯

#AgenticDevelopment #GitHubIntegration #ClaudeCode #EngineeringManagement #AI #FutureOfWork

Ensuring Repeatable Agentic Results

After weeks of curiosity (and even some skepticism) about my "six-hour flight app build," I finally had a chance to document the process and the tools I use.

What started as a simple "how do you do this" request turned into something a bit more profound. Recording myself explaining the agentic stack forced me to confront a truth: We're not coding anymore. We're conducting.

My tech stack? Claude Flow, Claude Code, OpenAI Codex, Cursor, GitHub Codespaces, Neon, Railway, Doppler, Snyk, Trivy, CodeRabbit, Clerk, etc. But that's like saying a symphony is just instruments.

The real magic happens in the orchestration. Vision documents that become living touchstones. Product Requirements and Technical Architecture Docs that agents reference hundreds of times per build. Implementation plans that update themselves. Sprints & Phases with kickoff prompts, completion docs, and handoff protocols.

Each phase starts fresh. No context window exhaustion. No drift. Just clarity.

My canonical starting templates are designed to support GitHub Codespaces for virtual development (available from any machine at any time). They come pre-loaded with GitHub workflows that reinforce linters, security, code reviews, and more, and support out-of-the-box deployment pipelines for Docker, Azure, Railway, and more.

When it gets to swarms, it gets even more interesting. The swarms don't just execute what you tell them to do. They can debate among themselves. For example, you can ask three agents to tackle the same problem. A fourth synthesizes their approaches. It's ideation and peer review at machine speed.

The video walks through everything. The templates. The workflows. And why you should consider the Claude Flow framework from Reuven Cohen that enables true swarm intelligence.

But here's the uncomfortable truth: This isn't about the tools. It's about letting go.

Letting agents review each other's work. Letting workflows enforce standards, I might skip. Letting swarms find solutions I'd never consider.

After 25 years away from coding, I'm shipping software faster than ever. Not because I got better at programming. Because I learned to conduct instead of code.

This is where I stand today. But it's fluid and dynamic. As tools become available, I try to adopt them. And note that not all of these tools and frameworks may be suitable for you. Feel free to build your own orchestra.

But the future isn't about YOU writing better code. It's about you becoming a better conductor of an orchestra of agents who can research, design and code for you.

Carpe Agentem. 🎼

#AgenticDevelopment #SoftwareEngineering #AI #StartupLife #SyntheticLeverage

Swarms at 34,000 feet

Design partner meeting in 48 hours. The platform wasn't quite ready. So I decided to put my Claude Code swarm to work at 34,000 feet.

By the time we crossed Iceland, they'd built over 50 React components, a complete mock API set simulating three required enterprise integrations, and a full admin interface. Initial testing indicated the platform could handle 1,000+ concurrent users with sub-200ms response time.

The agents called it "an extraordinary feat of engineering prowess." I had to laugh at their self-congratulation (reminds me of that time they claimed "100% robust, guaranteed" code). But they weren't wrong about the output.

What typically takes 18 developer-days was compressed into 6 hours. Complete with a fully responsive front-end, MCP-powered extensions, third-party Enterprise SaaS app integration, customizable dashboards, multi-modal content delivery (including voice), enterprise security, and role-based access control. Fully documented. Comprehensive TDD with all tests passing. Clean linter reports. Secondary security checks passed. Production-ready Docker configs. Kubernetes orchestration. Even a full CI/CD pipeline.

All before the seat belt sign came back on.

The craziest part? While I reviewed their work over mediocre airline coffee, they were already implementing performance optimizations I hadn't explicitly asked for. Just like they always do.

Two days from now, when the design partner (hopefully) marvels at our development velocity, I'll tell them about my transatlantic engineering team.

Welcome to the age of synthetic leverage. Where your most productive office is a metal tube at cruising altitude.

Having built multiple startups ... having experienced this sort of time pressure many times before ... I've never experienced this sort of technology leverage. Ever. It's frankly thrilling.

Carpe Agentem ✈️

#AgenticDevelopment #StartupLife #AI #ProductDevelopment

The Power of Swarms

After ten months of building with AI agents, I crossed a milestone over the weekend: $18 million in equivalent developer output. That's over 150 person-years of development. But it was the swarms that delivered almost as much functioning software in the past two months as we had collectively delivered over the eight prior months.

But here's what the headlines miss about agent swarms.

While it's right to celebrate the economics and reflect on the exciting productivity metrics, what the headlines don't tell you is how fundamentally different swarm development feels.

Traditional coding is linear. You write, you debug, you deploy. One thread of consciousness attacking one problem at a time.

Swarm development is orchestral. Right now, thanks to Claude Code and the Claude Flow hive framework from Reuven Cohen, I have 12 agents working in parallel: • 3 refactoring our LLM observability platform • 4 building new features for a new Breakfast with AI app • 2 writing documentation • 3 running security audits before the code is approved for release.

They're not just following instructions. They're "reasoning", debating, and course-correcting. One agent identifies a performance bottleneck, alerts another, and then spins up a third to benchmark alternatives.

The cognitive load shift is profound. I've gone from writing code to conducting symphonies (or sports teams).

But here's the part that keeps me up at night: We're not even close to the ceiling. We're still battling with some serious limitations:

🧠 Limited context windows (even at 200k tokens)

🔄 Not quite getting it right the first time

💰 Compute costs at scale

🎯 Focus drift in complex, long-running tasks

We're solving these systematically. New orchestration frameworks. Better memory systems. Smarter agent hierarchies.

The next milestone? $100M in output by year-end. Not because I'm chasing numbers, but because each breakthrough unlocks new possibilities.

Three months ago, a board member asked me: "Why do we need 150 developers?". It was a good question.

Today, the question isn't whether agent swarms will transform software development. The question is whether you will be conducting the orchestra or watching from the sidelines.

To my fellow technical founders: If you haven't experienced swarm development yet, expose yourself to it fast. This isn't the future of coding anymore. It's Tuesday afternoon in my home office.

Welcome to the age of synthetic leverage.

Carpe Agentem.

#AI #AgenticDevelopment #SoftwareEngineering #FutureOfWork #Innovation

Balancing the Risks and the Rewards of AI

We're facing one of the most important risk vs reward debates of our time.

Following on from my recent discussions with boards and C-level peers, it's pretty clear that AI is reshaping most enterprises. It's accelerating productivity, transforming processes, and redefining entire business models. The potential is immense, compelling, and impossible to ignore.

But navigating this new terrain comes with real complexity.

We face a paradox: the same AI technologies driving innovation are also amplifying risk. Confidential data leaks, biased decisions, regulatory penalties, and novel cybersecurity threats aren’t hypothetical—they’re here, and they’re growing. High-profile incidents have shown how quickly AI can become a liability rather than an asset.

Regulators have noticed. The EU’s AI Act, coming into force this week, mandates rigorous oversight for high-risk AI applications, requiring transparency, bias audits, clear accountability, and human oversight. Similarly, the other jurisdictions are rolling out comprehensive AI risk management frameworks.

Governance of AI is no longer optional; it’s essential.

The solution isn’t to slow down innovation but to accelerate it safely. This is where AI Observability platforms come into play.

AI Observability is about transparency, visibility, and control. It’s the critical layer that turns AI’s ‘black box’ into a transparent, manageable system, providing real-time monitoring, anomaly detection, bias mitigation, and compliance enforcement. It empowers senior leaders to trust their AI investments, confidently innovate, and swiftly adapt to evolving regulations.

Companies that master AI Observability will hold a distinct competitive advantage. They’ll innovate faster, mitigate risks proactively, and earn trust with regulators, customers, and partners.

Observability isn’t just risk management; it’s strategic enablement. And it's one of our key areas of focus at GALLOS Technologies.

#AI #Observability #Governance #Innovation

Swarms Deliver Powerful Returns

Well, it's the end of another month, and it's time to check in on what the agents collectively have been up to.

TLDR: We have now delivered almost as much software in the past two months as in the prior eight months. And this is not just de novo creation (aka vibe coding), a significant portion is refactoring and extending a complex enterprise-scale LLM Observability app (which is still in stealth). And the pace is only increasing.

So what has caused this spike in productivity?

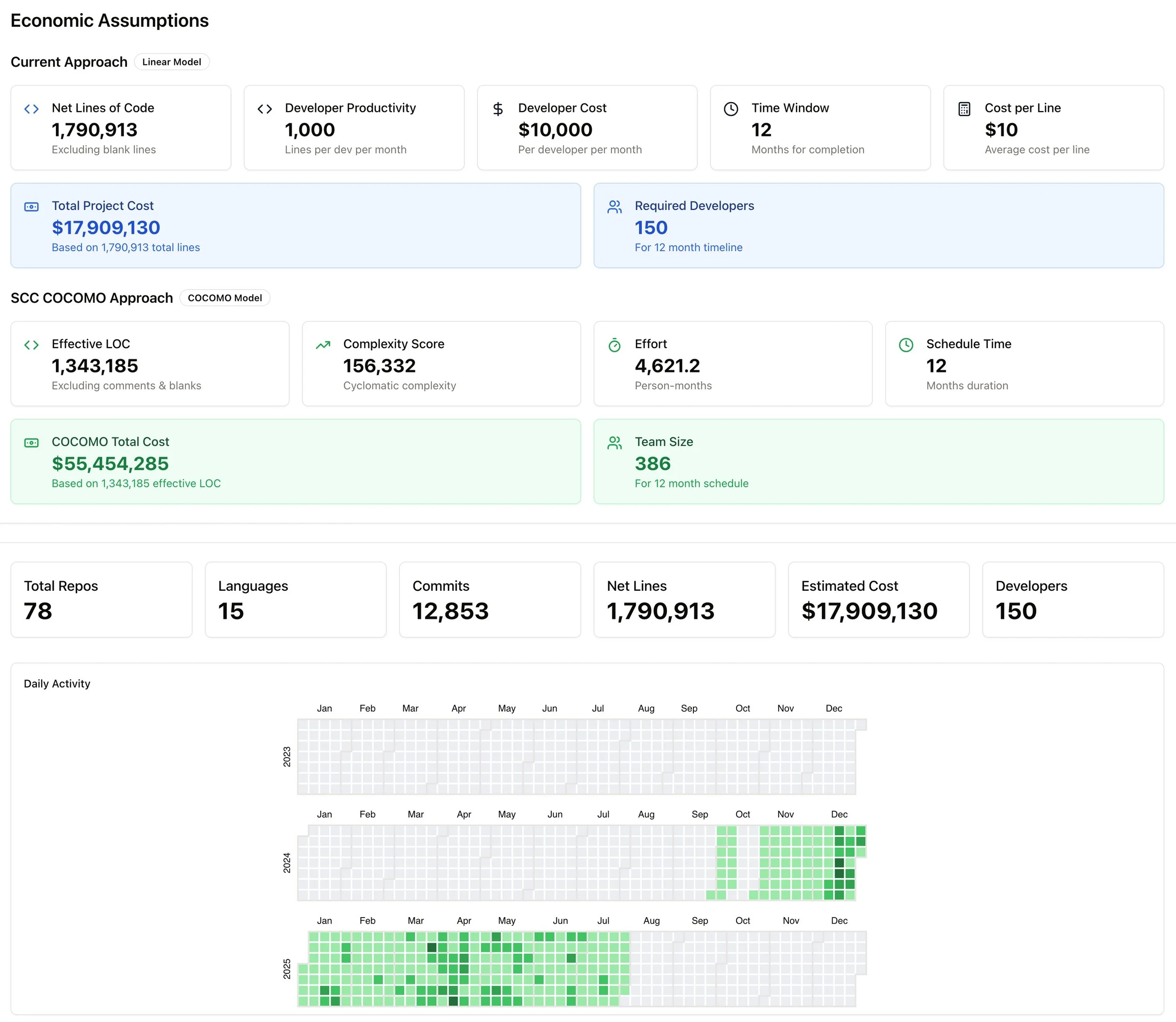

As I've moved more to swarm-based development, the velocity of what I'm able to produce has increased tremendously. The agents and I have seen a significant increase from approximately $11 million of equivalent developer output (lifetime-to-date) two months ago, to almost $18 million today.

Remembering that we started this journey in late September 2024, it took about eight months to get to $11 million, and only two months to get to $18 million. My estimates put that at 150 person-years of development so far.

Welcome to the economic leverage you can obtain from agent swarms.

This time, in addition to the approach that I've been following for the last few months, I've added a more industry-standard, SCC COCOMO approach as a comparator. This model is more sophisticated than mine and takes into account code complexity, etc.

The SCC COCOMO model, however, estimates a far higher equivalent of $55 million and over 380 person-years of output.

Hmmm ... that seems a bit outlandish ... so I'm going to stick with my more conservative approach for now.

But it just doesn't matter. The economic leverage is clear. The joy of coding again, though, is priceless.

Carpe Agentem

Coding Swarms Hit Mainstream

Starting to gain familiarity with, and get real traction from, Reuven Cohen's Claude-flow swarm technology; building and refactoring complex things with incredible velocity.

Once you have experienced this taste of the future of agentic software development, there is no going back. It's every technical founder's dream ... software at the speed of thought.

I suggest you follow the Agentics Foundation for exposure to some crazy smart people who are quite literally building the future of software development.

#Agentics

Resistance is Futile

Over the past few weeks, I have spent time walking several of my current and former board members, as well as some of my former leadership teams, through the current state-of-the-art in agentic development. Not because they need to learn to code, but because they need to understand why their entire business models might be obsolete in 18 months.

After over 25 years as a CEO, having lived through the internet, mobile, social, and fintech revolutions, I thought I'd seen every disruption. But when I returned to coding eight months ago, building 60+ apps that would have cost well over $10.8M in engineering spend, for less than $10,000, I realized: This isn't just another tech shift. It's the end of the software business as we know it.

When I demonstrate how I routinely now deliver hundreds of thousands of dollars' worth of equivalent developer productivity in 48 hours for $25 in compute costs, the room often goes silent.

When they push back with the same tropes of "well, that is not production code", I point out that two of my apps are now heading into production in G2000 companies; furthermore, these are companies in sensitive & regulated industries. These apps are at the heart of two exciting startups. AI is being used to create production code today in companies such as Microsoft, Salesforce, Oracle. Anthropic, OpenAI, Google, and Facebook. Don't for one moment cling to the notion that it is not production-capable. That comes down to how you use AI, not if you use AI.

One director finally asked: 'So... why do we have 150 developers?'

It's a good question. When one founder + AI agents outperforms a 10-person team at 1/100th the cost, every assumption about scale, hiring, and capital needs needs to be rethought.

Time is of the essence. Many boards are now planning for 2026. AI is revolutionizing next Tuesday. That disconnect will kill companies.

I often point out to the skeptics that their competitors aren't just adopting AI, they're being rebuilt by it. Reimagined by it. Reinvented by it. Rejuvenated by it. If a board doesn't understand agentic development, they're already behind.

Again, I'm not suggesting every board member learn to code. I'm saying they need to understand how AI agents work, what they can build, and why traditional planning cycles are now measured in weeks, not years.

So, talk to your boards about this... show them the art of what's now possible. Because the companies that thrive won't be the ones that merely adopt AI, they'll be the ones whose leadership truly grasps its potential.

Unleashing your AI CPO

A few weeks ago, I had a discussion about "table top exercises" and their utility in helping train internal teams to respond to cyber attacks. I was curious about space and so I had the agents build a very simple app that helped companies customize table top exercises, execute them with their teams, and score the responses.

For this weekend's breakfast with AI, I asked the agents to dream further ... to imagine far beyond what they had built and come up with something that would have no competitive peer in the industry.

I basically turned them into Chief Product Officers, and gave them the mandate of building something unique.

What they came up with was pretty interesting, and will be the topic of my next "Breakfast with AI" video:

⚔️ AI-Powered Red Team Integration: Dynamic adversary simulation with configurable threat actors (nation-state, ransomware groups, insider threats) that adapt tactics based on defensive responses

🌊 Cascading Incident Simulation: Multi-system failure modelling across supply chains, market-wide events, and infrastructure with real-time financial impact calculations

🏢 Physical-Cyber Convergence: Integrated physical and cybersecurity crisis simulation addressing facility security, manufacturing floor attacks, and critical infrastructure

🤝 Multi-Organization Coordination: Complete inter-company crisis coordination with regulatory authorities, law enforcement, media, and vendor relationships

🗣️ Advanced Voice Crisis Simulations: Real-time multi-character conversations with specialized AI personas (Physical Security Director, Facilities Manager, Emergency Coordinator)

🎯 Strategic Decision Analysis: Executive-level crisis decision simulation with financial impact modelling, regulatory compliance, and business continuity trade-offs

🎯 Live Crisis Command Center Emulation: Professional-grade real-time crisis coordination dashboard, with executive-level visibility across multiple organizations during active incidents with threat level monitoring and financial impact tracking

🧠 Predictive Crisis Intelligence: Machine learning models that forecast team performance degradation 30 minutes in advance with confidence intervals

📊 Readiness Analytics Dashboard: Comprehensive ML-powered performance tracking with organizational resilience scoring and industry benchmarking

And it actually runs ...

Could what started as a thought experiment, have now evolved into the world's most advanced crisis training application?

This experience was wild ...

"Breakfast with AI" projects like this show me what's possible when we combine human curiosity and vision with AI-powered research and code generation.

Thrilling ... for me at least.

Video coming next week.

There's Never Been a Better Time to Create

The founder journey used to be predictable in its unpredictability. You'd code in basements, bootstrap until you couldn't, raise capital, scale teams, fight fires, and if you survived the 90% failure rate, you'd build something meaningful.

After 25 years of this dance, leading teams of 5 people in a basement to 3,500 across 17 countries, I thought I'd seen it all.

Then I picked up coding again after a quarter-century hiatus, and what I discovered fundamentally rewrites the founder playbook.

In 1999, launching a tech company meant assembling armies. You needed developers, designers, QA teams, project managers, and documentation writers. Months to ship an MVP. Years to iterate. Millions in burn rate before you knew if anyone cared.

Agentic coding just turned this upside down.

Over the past 8 months, I've created over 60 apps, or about $10.8MM worth of software, for roughly $10,000 in compute costs. That's it. Period.

That's not a typo. That's a paradigm shift.

What Changes:

🚀 Speed of Validation Old world: 6-12 months to test an idea. AI world: 6-12 days to ship working software. The founder's greatest enemy has always been time. Now we can validate ideas at the speed of thought. "Fail fast" has become "fail instantly," and that's liberating.

💡 The Solo Founder Renaissance: Remember when VCs wouldn't touch solo founders? That bias may diminish. One founder with AI agents can now outpace traditional 10-person teams. The economics are undeniable.

🧠 From Managing People to Managing Intelligence: The skillset shifts from recruiting and retaining talent to orchestrating AI capabilities. Your agents don't need equity, don't burn out, and code while you sleep. But they need precise direction, thoughtful prompting, and strategic oversight.

📊 Capital Efficiency on Steroids: We used to measure burn rate in millions per month. Now? Build first, raise later. Or maybe never. When you can prototype for the cost of a used car, the entire venture model needs rethinking.

🎯 Hyper-Verticalization Becomes Viable: That niche market of 1,000 customers? Previously uneconomical. Now? Build bespoke solutions for micro-verticals. The long tail of software is about to explode.

But Here's What Doesn't Change:

That founder madness I wrote about a few weeks ago. Still essential. Maybe more so. Because while AI handles the mechanical, you still need:

1. The vision to see what others miss

2. The courage to challenge incumbents

3. The persistence to push through the "no's"

4. The wisdom to know when to pivot

AI doesn't replace founder instinct. It amplifies it.

The tools are here. The economics work. The only question is whether you have the founder madness to seize this moment.

After 25 years of building the old way, I can tell you with certainty: There's never been a better time to be a founder.

The future isn't coming. It's compiling.

Carpe Diem.

AI's Reimagine the Future of Banking

Last week, 𝘄𝗲 𝗹𝗲𝘁 𝗔𝗜 𝘁𝗮𝗸𝗲 𝗳𝘂𝗹𝗹 𝗰𝗿𝗲𝗮𝘁𝗶𝘃𝗲 𝗰𝗼𝗻𝘁𝗿𝗼𝗹 𝗼𝗳 𝗱𝗲𝘀𝗶𝗴𝗻𝗶𝗻𝗴 𝗮 𝗴𝗮𝗺𝗲 - from concept to characters to soundtrack to gameplay.

This week, we challenged them with something even bigger: 𝗿𝗲𝗶𝗺𝗮𝗴𝗶𝗻𝗶𝗻𝗴 𝘁𝗵𝗲 𝗳𝘂𝘁𝘂𝗿𝗲 𝗼𝗳 𝗯𝗮𝗻𝗸𝗶𝗻𝗴.

They came up with 𝗡𝗲𝘂𝗿𝗼𝗕𝗮𝗻𝗸, 𝗮𝗻 𝗔𝗜-𝗱𝗿𝗶𝘃𝗲𝗻 𝗳𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗲𝗰𝗼𝘀𝘆𝘀𝘁𝗲𝗺 𝘄𝗵𝗲𝗿𝗲 𝗮𝘂𝘁𝗼𝗺𝗮𝘁𝗶𝗼𝗻 𝗱𝗼𝗲𝘀 𝘁𝗵𝗲 𝗵𝗲𝗮𝘃𝘆 𝗹𝗶𝗳𝘁𝗶𝗻𝗴, 𝗮𝗻𝗱 𝗽𝗲𝗿𝘀𝗼𝗻𝗮𝗹 𝗳𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝘀𝘁𝗿𝗮𝘁𝗲𝗴𝘆 𝘁𝗮𝗸𝗲𝘀 𝗰𝗲𝗻𝘁𝗿𝗲 𝘀𝘁𝗮𝗴𝗲.

Forget manual transactions. Imagine a world where your 𝗽𝗲𝗿𝘀𝗼𝗻𝗮𝗹 𝗔𝗜 𝗮𝗴𝗲𝗻𝘁𝘀 optimize savings, manage investments, analyze spending patterns, and pay bills seamlessly, while offering 𝗳𝗼𝗿𝘄𝗮𝗿𝗱-𝘁𝗵𝗶𝗻𝗸𝗶𝗻𝗴 𝗳𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗶𝗻𝘀𝗶𝗴𝗵𝘁𝘀 tailored to you.

But it didn’t stop there. NeuroBank redefines the way we interact with money, making banking 𝗽𝗿𝗲𝗱𝗶𝗰𝘁𝗶𝘃𝗲, 𝘀𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰, and even 𝗰𝗼𝗻𝘃𝗲𝗿𝘀𝗮𝘁𝗶𝗼𝗻𝗮𝗹𝗹𝘆 𝗶𝗻𝘁𝗲𝗿𝗮𝗰𝘁𝗶𝘃𝗲.

Could this be the model for the future?

The agents thought so.